-

SEED produces a higher yielding and more diversified fixed income portfolio by diverging from a simple index approach.

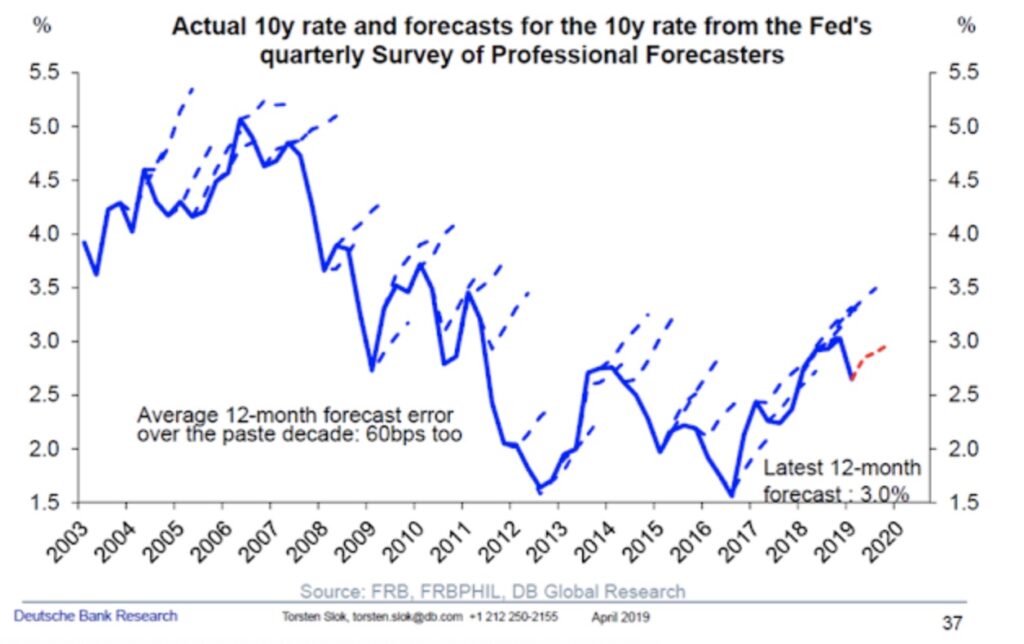

Basic bond math is straightforward (even harder concepts like duration and convexity are simple calculus), and the emergence of exchange traded funds (ETF’s) have given investors an equally straightforward and often adequate avenue to gain fixed income exposure. Like trying to market time the equity market, attempting to predict longer term interest rates has proven to be a fruitless strategy for individual investor and managers alike. That doesn’t mean we don’t take yield into account. As we discuss in 2016 “Interest Rates and Value Investing” then again in 2023 “Is Now a Good Time to Buy Bonds?“, often low yields indicate negative expected returns after inflation. We have avoided longer fixed-rate bonds in favor of floating rates bonds in those periods.

In general, we also avoid many bonds like Treasuries that have very lower expected returns as many investors are willing to pay a premium for liquidity. We like to be paid to give up that liquidity as we discuss in our 2020 article “Do Treasuries Have a Place in a Modern Portfolio?” We also recognize that unlike investing in stocks, the ability to invest in a truly broad index bond fund, is limited.

Broad fixed income index ETFs exist and are cost efficient; however, the sectors in which they invest cover only a fraction of the investable fixed income universe, leaving out sectors like leverage loans, much foreign debt (including emerging markets), below investment grade bond and junior subordinated debt, private or 144A credit, and private-label mortgage backed securities (MBS). Almost all of these sectors offer higher yields to investors (and yes, less liquidity). The average fixed income index ETF is comprised mostly of low-yielding government or agency bonds – roughly 45% government or agency debentures and 20% Agency MBS (which, after adjusting for their prepayment optionality, have only slightly higher yields than comparable treasuries.) In other words, the overall realizable yield in ETF’s and index funds is paltry and diversification across the fixed income market is lacking.

Of course, yield as a sole concept of value is misleading and, by investing in several more narrowly focused ETFs, investors can gain exposure to a broader array of fixed income asset classes. However, not all fixed income sectors will be covered and the cost will be significantly higher (roughly 5x or ½ a percent vs 1/10th a percent). And notably, there is no real passive, inexpensive way to own private label MBS. That fact may not matter so much when fixed income is used as a balance against equities (see section on Asset Allocation) or matching a known need (see section on Individual Bonds). But for many, especially retirees, this lack of exposure to the full array of fixed income products is limiting.

We can produce a higher yielding and more diversified fixed income portfolio by investing in a combination of individual bonds, more targeted ETFs/mutual funds and more targeted closed- end funds. We have also invested in Preferred Shares, Master Limited Partnerships (MLPs) and Real Estate Investment Trusts (REITs), viewing these assets as more fixed income like given their higher yields but with much more volatility and risk (see section on Fixed Income Substitutes). For closed-end funds and REITs, as we discuss in the sections set forth below, the high fees can be offset when either is purchased at a large discount to net asset value (NAV) or book value and is often mitigated by the fact that many funds calculate fees using net assets when they in fact manage a much larger portfolio through leverage (e.g., gross assets).